Credit Scoring Series Part Ten: The Bigger Picture – Enterprise Decision Management Systems

The previous articles in this series described the key elements of a robust credit scoring toolkit, including scorecard modeling, scoring strategy, implementation, and monitoring. By putting these pieces together, we can start building a bigger picture of the enterprise decision management (EDM) system. However, this is still insufficient for executing the complete credit-risk decision process. Making the full EDM picture requires bringing additional pieces together, including customer application processing, internal and external data gathering, policy rules, additional analytical models for fraud detection and risk management, optimization, overrides, and more.

With its three fundamental components: data, logic, and interface, an EDM system provides the framework for translating data into actionable decisions using data-, model-, knowledge-, communication-, and document-driven decision-making processes. A decision management system is only valuable if it can fulfill the following:

- Automation

- Data and systems security

- Process concurrency

- Scalability, (the capacity to handle a growing amount of processes that are both easy to change and extend)

- Transparency (so technical and non-technical professionals can understand, share, assess and audit business processes)

- Heterogeneity with diversity of data sources, synchronous and asynchronous processes, both local and remote

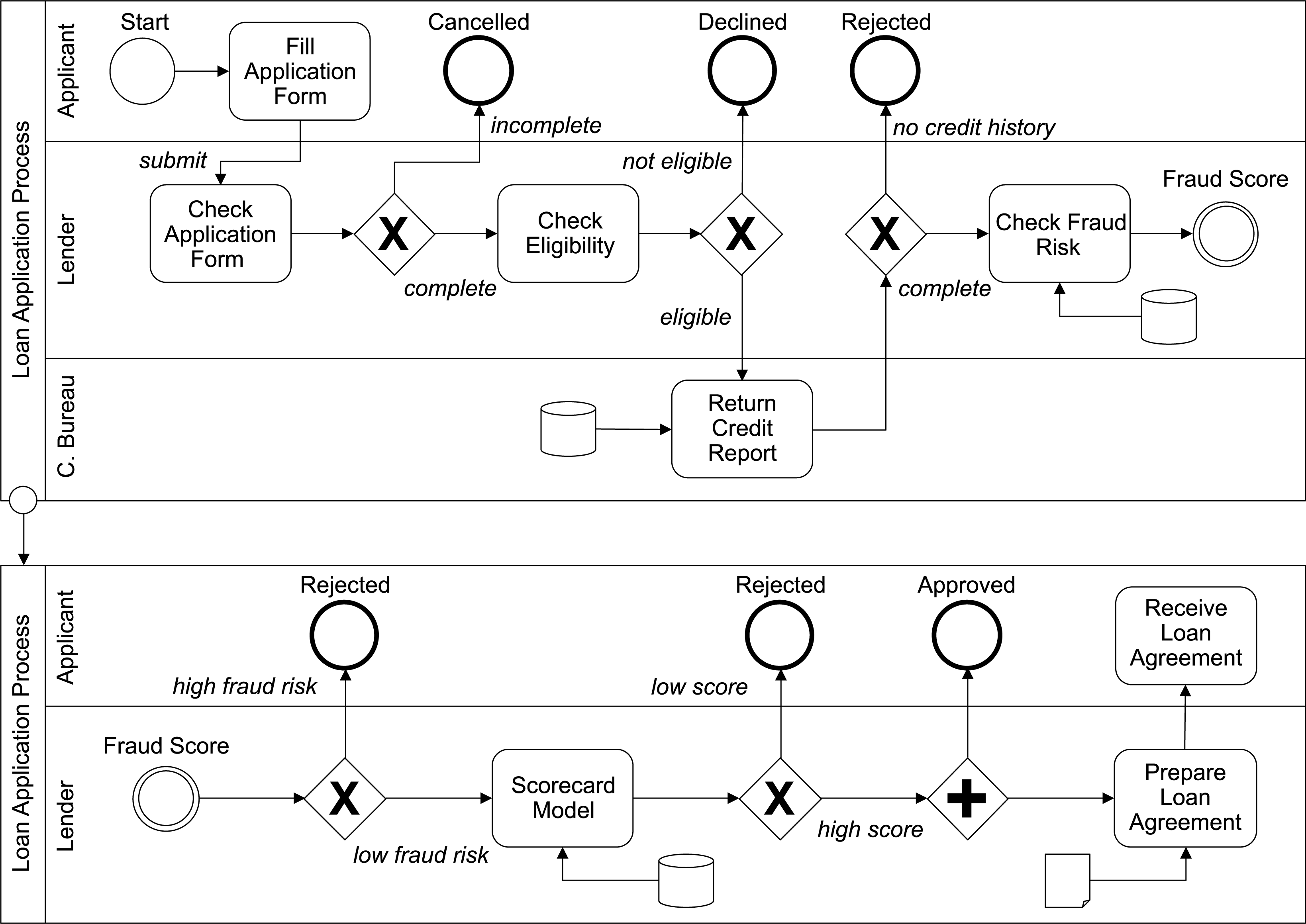

Business decisions are the key outputs of an EDM system. Decisions are consumed within a business process flow and can be reused in other processes. A mix of business rules and advanced analytics is typically considered when creating a decision requirements diagram for credit risk (Figure 1).

Business rules can be extensive encompassing internal and external policies, regulations, and best practices; typical examples of business rules include age requirements, employment status, credit history, bankruptcy and write-off history, different fraud rules, in-house records on exiting products, and more.

Overrides are a form of business decision that can overrule decisions based on a credit score cutoff value. Overrides can either approve applications that the score cutoff would’ve otherwise rejected, or reject applicants who would’ve been scored above the score cutoff. Overriding decisions are based on specific company rules and exclusion criteria.

Many predictive models can be utilized within a business process flow assessing various risk elements, such as fraud, delinquency, default and churn, or calculating applicants’ affordability and lifetime value. In addition, many optimization levels can be added in the process flow considering different objective functions such as minimizing operational cost or maximizing the margin. Return on investment (ROI) analysis – measuring the impact of business decisions – can also be the part of the business process, informing the optimal decision strategy.

Model management and monitoring are also important components of an EDM system. For improved decision-making, advanced business processes may incorporate adaptive analytic techniques by using model monitoring capabilities and machine learning algorithms. Any performance degradation of existing predictive models is captured using the model monitoring capability that, in turn, provides automated feedback into machine learning models, enabling real-time self-correction. This can significantly shorten a change management cycle and improve the decision-making process.

The complete credit risk decision process can be fully customized and proprietary to a financial institution. This, however, carries many risks, including complex system maintenance, human resources, and high cost. An alternative solution would be to opt-in using a commercial EDM system that would be faster to implement, require less resources and drive cost efficiencies through investment in technology.

Commercial EDM systems are typically equipped with visual programming features and a point-and-click user interface enabling data scientist or business analysts with no programming skills to create decision requirements diagrams, specify input parameters, control model outputs, implement business rules, run processes in parallel or direct outputs to other internal or external processes.

Ease of implementation, speed of change, compliance with regulations, and components modularity are some of the great benefits of EDM systems. They are the brain of a complex body that orchestrates its single components, creating a harmonic business symphony.

Conclusion

With this, we end the Credit Scoring series that demonstrated the development journey from start to finish. Thank you for reading, and please reach out to our representatives if you’d like to learn more or set up a call with experts ready to help you take the next step in your credit risk journey.

Read prior Credit Scoring Series installments:

- Part One: Introduction to Credit Scoring

- Part Two: Scorecard Modeling Methodology

- Part Three: Data Preparation and Exploratory Data Analysis

- Part Four: Variable Selection

- Part Five: Credit Scorecard Development

- Part Six: Segmentation and Reject Inference

- Part Seven: Additional Credit Risk Modeling Considerations

- Part Eight: Credit Risk Strategies

- Part Nine: Scorecard Implementation - Deployment, Production, and Monitoring